I’m this close to sending out a buy call on a stock that—if I do—I know would light up the phone lines (and customer-service inbox!) at our New York office.

There’s a good reason why: Imagine being along for this drop.

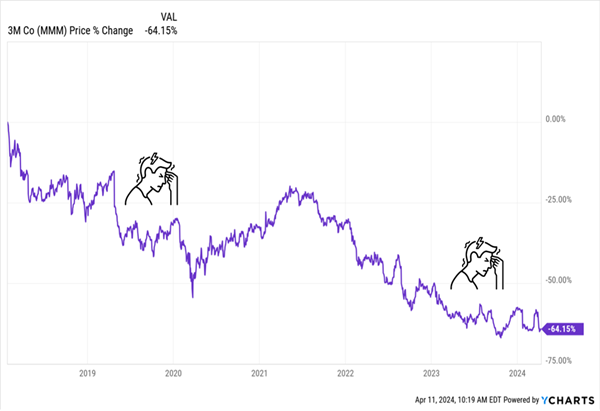

New “Watch-List” Addition Sheds Two-Thirds of Its Value

(Heck, given that this stock was till recently a staple of many dividend portfolios, maybe you don’t have to imagine.)

That’s the peak-to-trough dive on 3M Co. (MMM) in the last six years. To put it in perspective, it came as the broader S&P 500 gained 79%.

I know that buying—or even considering—a stock with a chart like this gives many folks heart palpitations. But “dumpster-dive” moments like these are often the best time to buy. And make no mistake, 3M has stepped on every banana peel (and garden rake!) there is.

Right now it’s facing:

- A legal “overhang”: Last year, management agreed to pay $16 billion to settle two lawsuits (more on those below).

- A potential dividend cut: The stock yields a high 6.5% and has raised its payout for 64 years. But that streak may end on or before February 2025, the next time it’s due to announce a hike.

A cut, or a failure to hike, would drop 3M out of the Dividend Aristocrats, the 68 S&P 500 stocks that have raised their dividends for 25 years or more.

I know what you’re thinking: “Brett, you’re really considering buying a stock with a possible dividend cut ahead?”

This situation reminds me of the words of Howard Marks, the most successful value investor no one has ever heard of (except Warren Buffett, who’s a fan). Marks wrote:

“The ultimately most profitable investment actions are by definition contrarian: you’re buying when everyone else is selling (and the price is thus low) or you’re selling when everyone else is buying (and the price is high).”

But he admits this isn’t easy:

“These actions are lonely and uncomfortable.”

Let’s get into our turnaround case, starting with 3M’s main strength: a ton of brand loyalty. In all, the company peddles 12,000+ home-and-workplace staples under a bevy of labels, including Scotch, Post-It and Filtrete.

This, by the way, is one reason why Wall Street hates 3M: With a product list larger than the population of a decent-sized town, it’s always been tough to value. Much easier for the suits to keep track of the five models offered by Tesla (TSLA)!

Cue the Reboot

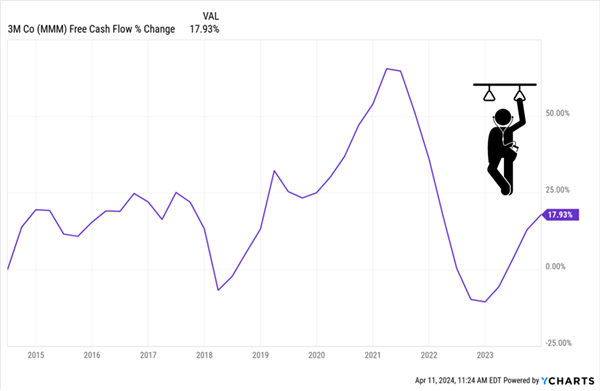

That leads us to 3M’s free cash flow (FCF), which is our go-to profitability metric when looking at any dividend-payer because unlike earnings per share, FCF can’t be manipulated by accounting.

In the last year, FCF was healthy, at $5.1 billion.

FCF did take a hit during the pandemic. But that was then. Nowadays, being in the office (at least a few days a week) is back, baby! In New York, some 80% of workers have been safely returned to their cubicles, according to Bloomberg.

That’s just starting to show up in 3M’s FCF:

3M’s Cash Flow Rises as Offices Fill Up

What’s more, 3M is taking steps to put its other woes in the rear-view.

3M Can Handle Its Legal Issues

Last year, the company settled two lawsuits—one over earplugs it sold to the US military and another over its use of so-called “forever chemicals,” which don’t break down easily, found in drinking water. As mentioned, the total bill was $16 billion.

That’s a big number, of course—and it’s why the last few hangers-on have thrown in the towel on the stock.

But this seemingly heavy burden really isn’t that bad: 3M has 13 years to pay the $10-billion chemical settlement. That’s around $800 million a year. The earplug agreement will be up to $6 billion paid over seven years between 2023 and 2029.

3M’s FCF can easily handle these costs, and that’s before accounting for any growth, which, as we just saw, looks like it’s starting to kick in.

Investors Often Put Too Much Focus on Legal Woes

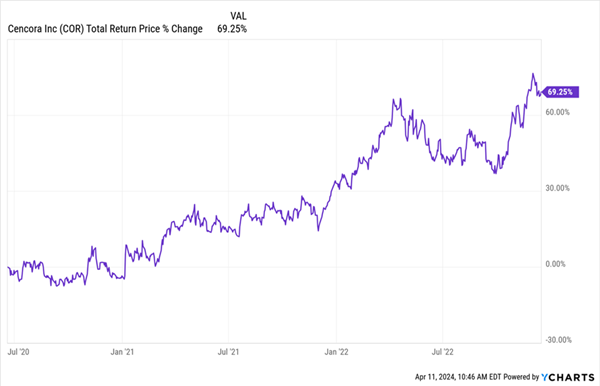

This story reminds me of AmeriSource Bergen, since rebranded to Cencora (COR)—who picks these names?—a drug distributor we recommended in my Hidden Yields service in June 2020.

AmeriSource’s shares then, like 3M’s now, were weighed down by litigation, in its case related to the opioid crisis.

But from a purely investment standpoint, worries about the $25-billion settlement (split between ABC and two other drug distributors) were overdone. As with 3M, ABC’s portion of the settlement was payable over a long time—18 years, to be exact. The net effect on FCF was less than 25%.

So we bought. And when we sold in December 2022, we took home a 69% total return.

A 69% Return in Less Than 3 Years

Next, let’s talk about the recent spinoff of 3M’s medical-devices business, now called Solventum (SOLV). The spinoff will streamline 3M. It will also shave about $700 million to $800 million off the parent firm’s FCF.

On the plus side, Solventum took $8.3 billion of the parent firm’s debt with it, lowering future borrowing costs. Rising office-product demand will help 3M’s cash flow, too.

As a result of these worries, MMM trades at just 1.6-times sales, just over half its five-year average of 2.6! Which brings us to that 6.5% dividend.

Let’s Let the Payout Dictate Our Next Move

Finally, the dividend—which is the one reason we’re holding off on a buy here. The upshot here is that a cut has been priced in. And we can be relatively sure that any cut would be “one and done.”

Chief financial officers are like carpenters. It’s best to measure twice and cut only once.

As a result, the safest dividend is often the one that has recently been cut. Unless management is a clown show (and 3M’s is not), the last thing they want is to have to cut twice when they had to be strapped to the gurney to do it once!

3M would be a good buy before a dividend cut. But it could be a great buy after one (or after it gets booted from the Aristocrats). Let’s let the spinoff dust settle and give management time to sort out its next dividend move. When (and if) the time is right, I’ll issue a buy call in Hidden Yields.

We’re NOT Waiting for 3M—Let’s Buy These 5 “Forever” Dividends Now

Even though I’m not quite ready to issue a buy call on 3M, it’s exactly the type of stock we want to own now: a proven, cash-generating business that’s been unfairly tossed in the bargain bin.

That way, if rates stay “higher for longer” and the market slips, these stocks’ cheap valuations will hedge our downside. And when rates (inevitably) fall, they’ll take off.

And we’ll enjoy their surging dividends the entire time!

As I said, I’m waiting for management’s decision on the dividend to make the final call on 3M. But that could take till next February, and we’re not waiting around.

Right now I’m urging investors to buy 5 other “recession-resistant” stocks with dividends that are not only growing but accelerating. That’s grabbing investors’ attention, and they’re bidding up these stocks’ prices in lockstep.

These 5 stocks—all Hidden Yields recommendations—are also (for now!) trading at bargain valuations, helping hedge our downside in a pullback and making them truly “recession-resistant” picks.

The bottom line: I’ve got these 5 picks pegged for 15%+ annualized total returns for years to come.

It’s time to make our move.

Click here and I’ll share more details on these 5 “recession-resistant” stocks and give you the opportunity to download a free Special Report revealing the names and tickers of each one.