It really is possible to find stocks that grow your money 15%+ a year forever—even in the middle of a pandemic.

Better still, these “unicorns” are a cinch to find. We only need to look for one thing: a dividend that’s growing—and ideally accelerating.

I know that sounds like a tall order, with S&P 500 payouts plunging $42.5 billion in the second quarter. But that figure masks the fact that many companies are still hiking their payouts—and will continue to, even if this crisis drags on longer than we expect.

Dividend Growth = Share-Price Growth

Of course, it’s not good enough to simply pick a few stocks with fast payout growth and call it a day. As we’ve seen in this crisis, many firms whose payouts were thought to be unassailable—like that of mall landlord Simon Property Group (SPG)—were slashed when the pandemic shuttered businesses.

We need to go further, carefully safety-checking our payouts to make sure their streaks can continue.

Further on, I’ll give you four simple indicators I use to make sure my payouts are safe. Bear in mind also that payout growth isn’t only critical for growing your income stream; it also grows your portfolio’s value, because nothing inflates a firm’s share price (and hedges its downside) better than a surging payout.

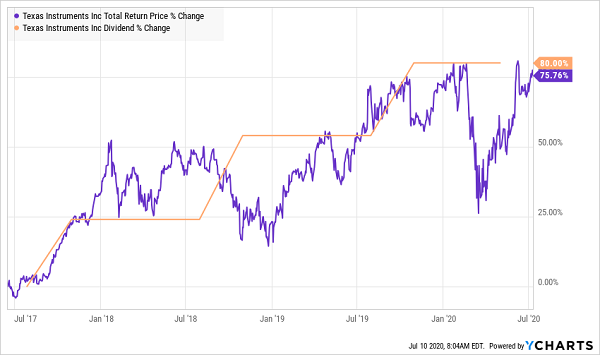

This Stock Delivered 80% Payout Growth—and Doubled the Market’s Gain

To see what I mean, consider chipmaker Texas Instruments (TXN), a company that members of my Hidden Yields service know well. I recommended TXN in June 2017, and it’s since returned 76% in gains and dividends, powered by an 80% jump in its payout. That’s more than double the S&P 500’s 37% return.

Take a look at this chart. The link between dividend and share price is clear.

Dividend Up, Share Price Up

The stock clearly jumps along with the dividend. That’s because investors know what they’re getting with TXN: CEO Rich Templeton, who’s filled various management roles for the firm since 1996, is a devoted dividend raiser, having hiked TXN’s payout for 16 years, straight through the 2008/09 crisis.

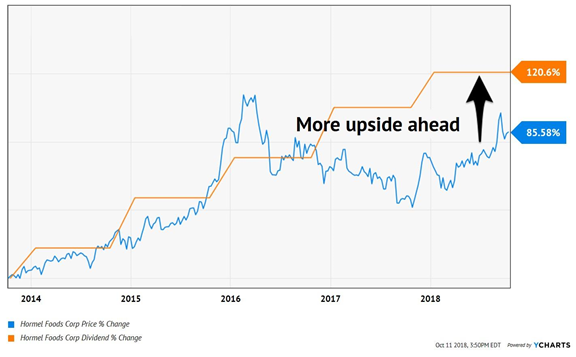

History Repeats With Hormel

This “dividends-up, share-price-up” pattern is no coincidence. I’ve seen it happen over and over, like with another stock I’ve recommended in Hidden Yields: Hormel Foods (HRL), whose canned and packaged fare was in high demand during the lockdown, helping the stock easily beat the S&P 500 year to date.

Steady Dividend Grower Wins in a Crisis

But let’s rewind to when I first recommended Hormel, in October 2018. Back then, I saw that its share price had tracked its payout higher until 2016, when it fell off the pace. That was our signal that Hormel was set for “snap-back” price upside as the situation righted itself:

Hormel’s Stock Was Set to Jump in Late ’18

What happened? Hormel has since delivered a 19% total return, with far less volatility than the S&P 500.

(By the way, I’ll give you my current buy-sell-hold recommendations on Hormel and Texas Instruments when you take a no-risk 60-day trial to Hidden Yields. You’ll also get a free report with my 7 top dividend-growth stocks to thrive in this pandemic and beyond. Full details here.)

Hormel’s Dividend Magnet Kicks In

Now that I’ve shown you the effect a rising dividend has on a stock, let’s dive into those four steps you can use to spot the next Texas Instruments or Hormel yourself.

Dividend Safety-Check #1: A Payout Ratio at (or Below) 50%

You’ve probably heard of the payout ratio—it’s the percentage of net income a company has paid out as dividends.

Most first-level investors use this formula without thinking—but we’re going to go a step further. That’s because net income is an accounting creation that can be manipulated, skewing the picture. Instead, we’ll use dividends as a percentage of free cash flow (FCF). We ideally want to see a ratio of 50% or less.

Both of our picks above easily met that mark: when I recommended Hormel, it was paying 46% of FCF as dividends. Texas Instruments? Just 46.5%.

Dividend Safety-Check #2: A Healthy Balance Sheet

There’s no hard and fast rule here, but ideally I like to see a company holding cash that’s a high percentage (or even greater than) its long-term debt and/or debt that’s half (or less) of assets.

And be on the lookout for truly of out-of-whack numbers here: for instance, if a company’s debt is higher than its market cap (or the value of its outstanding shares), avoid it entirely.

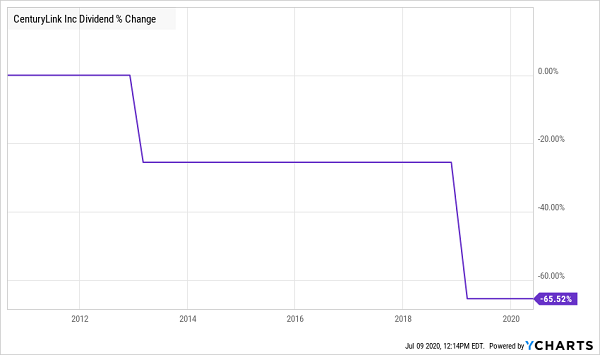

Dividend Safety-Check #3: A History of Payout Growth

It sounds like a no-brainer, but one of the best indicators of future payout growth is how a company has managed its dividend in the past. I especially like to see a payout that’s risen through a crisis, like the 2008/09 meltdown.

Hormel passes that test: it’s paid a dividend since becoming a public company in 1928, and has hiked its payout for 54 straight years. And we’ve already touched on Texas Instruments CEO Rich Templeton’s love of payout hikes: the chipmaker has pushed its payout higher for 16 consecutive years.

That stands in opposition to “sucker yields” like regional telco CenturyLink (CTL), which might tempt you with its 10.2% yield. But that high yield hides a toxic dividend history: this payout’s dropped nearly two-thirds in the last decade!

CenturyLink’s Dividend: A Retiree’s Nightmare

Let’s wrap with our final check of dividend safety—it’s one many first-level investors fail to check, even though you can uncover it with a quick Google search.

Dividend Safety-Check #4: High Insider Ownership (Including the CEO)

Buying a firm where management has skin in the game only makes sense. After all, if the C-suite owns a big slice of the company, they have every incentive to deliver strong returns (including fast-growing dividends!) to shareholders.

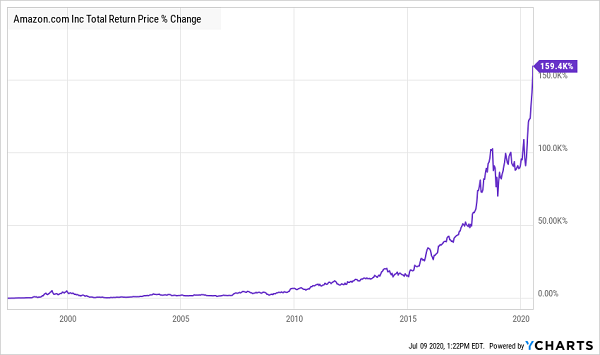

The classic example of a company with high insider ownership is Amazon.com (AMZN). According to the SEC, CEO Jeff Bezos owned 55.5 million shares as of June 30, about 11% of the e-commerce giant. Amazon’s performance since its IPO, which took place three years after Bezos founded the company in his garage, is a matter of record:

Amazon Enriches Bezos—and Shareholders

Of course, Amazon pays no dividend, so it’s disqualified for us income hounds. But many dividend growers do have CEOs with big ownership stakes, and these should definitely be on your radar. Rich Templeton, for example, personally owns 848,738 shares of Texas Instruments—a stake worth more than $108 million! So you can bet he’ll do everything he can to keep the share price—and dividend—rising.

Get First-Mover Advantage on My NEW Dividend Growth Pick—This Friday

I’d love to give you my full recommendation on Texas Instruments and Hormel right here, in this article, but to do so wouldn’t be fair to my paying Hidden Yields subscribers.

But don’t worry, I’m going to give you my latest buy-sell-hold call on these stocks, plus a whole lot more, too—including access to my latest dividend-growth pick, coming this Friday, July 17 (more on this in a moment).

It all comes your way with a no-risk, no-obligation 60-day trial to Hidden Yields, which I want to set you up with today. Your VIP trial gives you full access to my portfolio of 13 stout dividend growers, including my latest recommendations on both Texas Instruments and Hormel.

I’ll also give you that FREE special report I mentioned earlier—the one that names my 7 best dividend-growth stocks to buy for this crisis and beyond. They include:

- An under-the-radar income play that’s poised to double its payout and deliver 100%+ gains …

- Another company that’s raised its dividend by an astounding 295% over the past 10 years, and …

- A blue chip dividend grower set to boost profits by double digits in 2020!

AND you’ll be among the first to get my next issue of Hidden Yields, due out this Friday, featuring a brand-new dividend-growth pick. My recommendations tend to move up fast once they’re announced, so you’ll want to make sure you get in on this stock as soon as this issue is released.

To sum up: you get instant access to my Hidden Yields portfolio—including my latest buy-sell-hold advice on Hormel and Texas Instruments—a FREE report revealing my 7 favorite dividend growers and first-mover advantage on my newest Hidden Yields pick, set to roll out to subscribers on Friday morning.

Don’t miss out. Go right here to get this unrivaled income- (and portfolio-) growing package.