You’ve probably heard by now that investing just got a little bit cheaper. Now cheaper isn’t necessarily better, especially for those of us hunting for safe, meaningful yields to fund our retirements.

We’ll get to our diversified 3-click, 7.4%-yielding portfolio (including a couple monthly payers) in a moment. But first, more on the no-commission craze.

Following in the footsteps of Robinhood, Interactive Brokers (IBKR) announced a “Lite” version of its platform with commission-free stocks and ETFs. Then Charles Schwab (SCHW) announced it would offer commission-free stock, ETF and options trading, with TD Ameritrade (AMTD) and E*Trade (ETFC) in tow.

Online brokerages have been pushing selects sets of commission-free ETFs for some time. These recent moves give investors another reason to buy them.

Problem is, these funds are products of brilliant marketing teams rather than smart money managers. Exchange-traded funds don’t deliver nearly as much income as investors need to retire. Not even close.

Here are some truly ugly facts about the ETF industry that should give retirement investors second thoughts about leaping into these products now that they can save an extra buck or two. Out of the 100 most popular funds by assets under management (AUM) …

- None of them yield more than 7.7%—my “magic number” for a truly retirement-sustaining holding.

- Heck, none of them yield even 6%. The highest yielder comes in at just 5.6%!

- Less than a quarter of them yield more than 3%.

- Their average yield is a meager 2.5%. You can walk to your local bank and get that kind of income from a CD!

Of course, the only way a 2.5% yield makes any sense in retirement is if you’re sitting on a nest egg of about $2 million. But most people aren’t. Even if you’ve accumulated $1 million, the average ETF would pay you just $25,000 a year in annual income. That won’t be enough to even cover your bills in retirement, let alone all the extras that make retirement worth it!

And if you think high yields and hot performance are mutually exclusive, think again. The biggest closed-end funds (CEFs) have mere fractions of the assets of largest CEFs, and chances are you haven’t heard of them. But they punch well above their weight, outclassing the ETF world’s heavyweights:

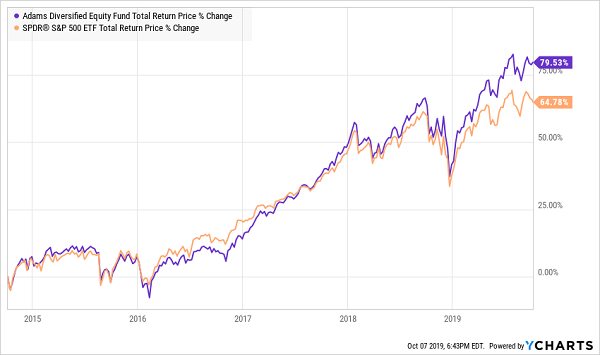

Broad Equity: SPDR S&P 500 ETF (SPY) vs. Adams Diversified Equity Fund (ADX)

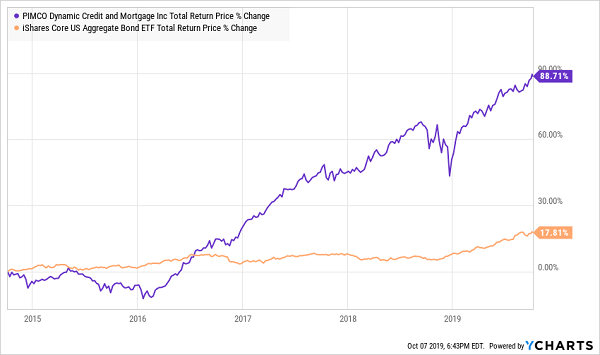

Diversified Bonds: iShares Core US Aggregate Bond ETF (AGG) vs. PIMCO Dynamic Credit and Mortgage (PCI)

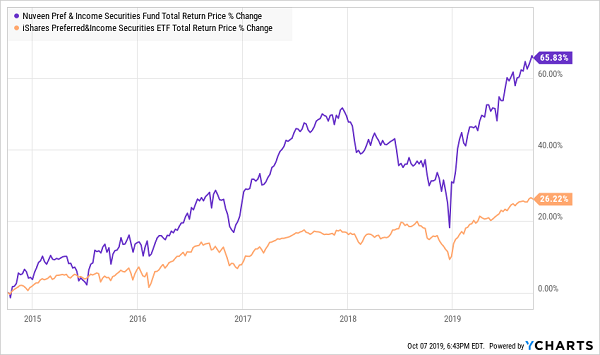

Preferreds: iShares Preferred and Income Securities ETF (PFF) vs. Nuveen Preferred & Income Securities Fund (JPS)

If your strategy in retirement is to fully fund yourself on income alone, any growth after that is just added security. When the unexpected happens, it’ll help to have a nest egg that can absorb a financial shock or two.

Let’s look at a few more CEFs that can put their ETF counterparts to shame while serving up gaudy yields up to 8.8%—including a pair that deliver those checks each and every month.

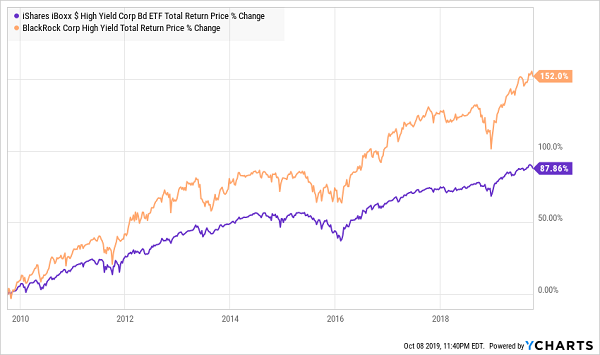

BlackRock Corporate High-Yield Fund (HYT)

Dividend Yield: 8.8%

Replaces This Popular ETF: iShares iBoxx $ High Yield Corporate Bond ETF (HYG)

Junk bonds. Non-investment-grade debt. High-yield bonds.

Whatever you want to call it, this is a perfect place to find yield, and to illustrate the disparity between ETFs and CEFs.

Bonds have broadly surged in 2019 amid a flight to safety. It’s one heckuva bonus for investors who were simply in fixed income for the steady paycheck. The iShares iBoxx $ High Yield Corporate Bond ETF’s (HYG) 10% total return year-to-date includes about 6 percentage points in price appreciation. Not bad for the roughly 1,000-bond index fund.

But HYG’s dispassionate, formula-driven index methodology has left a lot of money on the table—money that BlackRock Corporate High-Yield Fund’s (HYT) skilled managers have scooped up with both hands.

HYT boasts a slightly larger portfolio of about 1,100 debt issues hand-selected by James Keenan, Mitchell Garfin and Derek Schoenhofen, who are tasked not only with identifying top junk opportunities, but using leverage (a hefty 28% at present) to squeeze every ounce of return from those bonds.

Investors aren’t sacrificing much in the way of credit quality with HYT. And while the average duration is longer (4 years versus HYG’s 3), it’s still fairly short. The tradeoff is a significant upgrade in yield, at 8.8% compared to HYG’s 4.9%.

Not to mention considerably better performance over time.

BlackRock’s Active Managers Put Its Index Fund to Shame

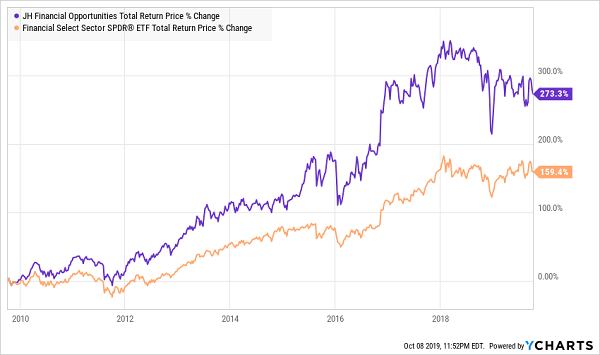

JH Financial Opportunities Fund (BTO)

Dividend Yield: 7.0%

Replaces This Popular ETF: Financial Select Sector SPDR Fund (XLF)

You’d never know it by reading financial media, but sector funds do exist outside of the SPDR family.

The JH Financial Opportunities Fund (BTO) is a comparatively niche fund to the SPDRs, boasting just $575 million in assets under management – literally less than 3% of what the Financial Select Sector SPDR Fund (XLF) puts to work.

But BTO has it where it counts.

Read the Scoreboard, SPDR

John Hancock’s fund and the SPDR offer roughly similar financial-sector exposure. But even a quick look at the crossover between XLF’s top five holdings and their weight in BTO can tell us so much about just how different they truly are.

Managers Lisa Welch, Susan Curry and Ryan Lentell, who boast a combined 79 years of experience, don’t stack most of the fund’s assets in Wall Street’s largest financials, unlike the market-cap weighted XLF. XLF’s big five account for more than 40% of the fund; they aren’t even a tenth of BTO’s assets.

John Hancock’s fund also is avoiding the tire fire at Wells Fargo (WFC). The lack of Berkshire Hathaway (BRK.B) is no mistake, either. While it indeed has insurance businesses, it’s hardly a pure financial, considering its ownership of companies such as Fruit of the Loom and See’s Candies, and stock holdings in Apple (AAPL) and Coca-Cola (KO).

BTO also turns the typically low-yielding financial sector into an income powerhouse. Its 7% yield is more than thrice the measly 2% XLF is doling out, and it’s paid monthly to boot.

I will point out, however, that BTO has underperformed over the past couple years. But that’s mostly an effect of its more concentrated focus. Pure banking index funds have similarly trailed the XLF. Renewed strength in the industry should elevate it once more.

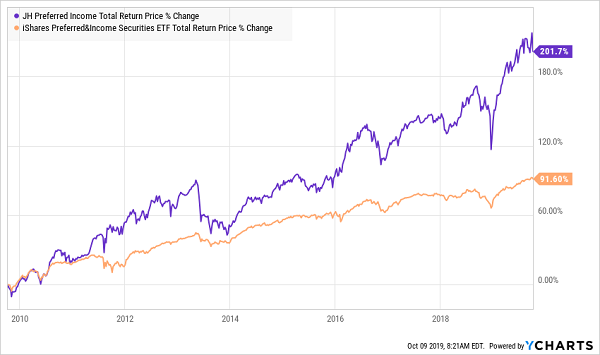

JH Preferred Income (HPI)

Dividend Yield: 6.4%

Replaces This Popular ETF: iShares Preferred and Income Securities ETF (PFF)

Preferred stocks are a can’t-miss source of yield. Companies use these stock-bond hybrids to raise funds with equity instead of digging themselves deeper into debt. But they still are on the hook for coupon-esque dividends, often in the range of 5%-7%.

Better still, even the most basic of preferred funds, such as the iShares Preferred and Income Securities ETF (PFF), deliver their distributions on a monthly basis.

But like bonds, preferred stocks don’t really offer much price “wiggle.” That makes it all the more important to find skilled managers who can identify misprinted issues and get the most out of this asset class.

JH Preferred Income (HPI) has done an excellent job of that over the years, more than doubling the ubiquitous preferred index fund’s total return over the past decade.

Don’t Invest in Preferred “Lite”

There’s no secret to the sauce. John Hancock’s Joseph Boyozan and Brad Lutz simply make the most of the tools at their disposal. Among them, significant leverage (34%) helps squeeze a 6%-plus yield out of this basket of fairly good-quality preferreds.

But it’s rare that a CEF gets this crowded. Over the past five years, JH Preferred Income has traded at an average discount to NAV of about 1%. At this very moment, it trades at an 8% premium, which is going to be a difficult barrier to outperformance going forward.

How to Collect $3,000 in Dividends Each and Every Month

These funds are close. They offer up high yields, and the two John Hancock funds even deliver their dividends monthly—a vital retirement-portfolio trait.

We’ll call them B+ picks. They very well could get you to the finish line.

But why take chances?

My “Monthly Dividend Superstars” tick off every checkbox in the retirement wish list:

- High annual yields nearing 8%. That translates into $3,125 in monthly income … on a nest egg of just $500,000. It’s all gravy from there if you’ve saved up even more.

- Real upside potential of about 10% annually. That will keep your nest egg growing in retirement, protecting it against any sudden financial “shocks.”

- Hidden value. There’s such a thing as “too popular.” If too many investors crowd into a stock, it becomes grossly overpriced, making more upside difficult to come by and increasing the risk of hyper-aggressive selling if investors get nervous. My “Dividend Superstars” are too small to be flush with institutional money, and far off the radar of many analysts, creating price inefficiencies that you and I can exploit.

This is the path less traveled. Most finance-TV pundits will tell you to sink your hard-earned retirement money into “can’t-miss” blue chips like the Dividend Aristocrats. They’ve grown their dividends for decades, and probably will for decades more.

Ignore their nonsense. Those same Dividend Aristocrats only yield about 2% on average, and the most established Aristocrats’ dividend growth has slowed to a sloth’s leisurely stroll. When you retire, your income stream will be so insufficient that you’ll be forced to hack away at your savings to pay your monthly bills.

Don’t take that gamble. Pay your monthly bills with outsize monthly dividend checks, and use the leftover cash to take a couple trips, build that backyard pool or spoil your grandkids rotten.

Let me show you the way to a set-it-and-forget-it 8% portfolio. Click here to get a FREE copy of my exclusive “Monthly Dividend Superstars” report, complete with tickers, buy prices, yields and analysis … as well as a other bonuses, including 12 popular dividend stocks that you need to SELL NOW before they ruin retirement.